As an alternative to paying with cash, credit, debit, or cheque, Dwolla makes it possible for companies to accept ACH payments. Customers can use ACH payments to deposit money directly from their bank accounts into your company bank account, and you can use ACH payments to return money to customers for credits and refunds.

Dwolla vs. Stripe:

Stripe: More individualized

A payment processor called Stripe also accepts ACH transactions. Processing ACH payments cost 0.8% of each transaction, up to a maximum of $5. For online payments, you may also handle credit card transactions at 2.9% + 30 cents.

The ability to create an embeddable checkout page, an invoicing platform, and a fraud protection system are additional capabilities. Additionally, because it is a pay-as-you-go payment processor, you can discontinue using the service whenever you choose.

Dwolla customer support: Your CIP-validated Dwolla Master Account may programmatically create a Dwolla API Customer using the Create a Customer endpoint. The Customer will engage directly with your application to manage their account after the API has processed all the necessary information. The developer should create the Customer type that best fits the use case of your application. Here is a very high-level breakdown of the several customers kinds that Dwolla offers. Customer Identification Programme (CIP) Verification is something to bear when choosing what kind of customer to generate for your application. Remember that a transfer between two parties necessitates that at least one party be CIP validated, regardless of your application type. Dwolla online help center for all users; dedicated support team available only with an annual contract for Scale plan or Custom plan.

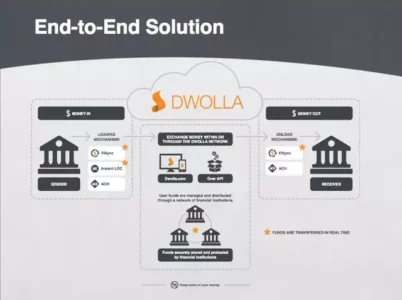

Dwolla payment processing: The typical clearing period from the Dwolla Network to a bank is between one and two business days. Before our cutoff time of 4 p.m., if a transfer is made, the money will be sent through the ACH Network for processing. When a transfer is made after our cutoff time of 4 p.m., the money will be taken out of the Dwolla Network the next day. Funds will be sent to the destination bank on the same day if exports from the Dwolla Network are upgraded to use same-day ACH clearing. As an illustration, money that leaves the Dwolla Network before 1 or 3 p.m. Central Time will be in the recipient’s bank account before the end of the day.

Dwolla merchant services: Dwolla is undoubtedly an intriguing choice if you’re an eCommerce shop seeking an ACH payment processing provider. A premium subscription will provide you access to a lot more features than you would with the ACH processing choices provided by the majority of conventional merchant service providers. Dwolla could be the right choice for some particular sorts of businesses.

Although the free Pay-As-You-Go plan can help you save a lot of money, you’ll have to handle all of the technical support choices and integrate Dwolla into your website.

Dwolla payment options: Businesses may accept ACH payments using Dwolla as an alternative to cash, credit, debit, or cheque payments. Customers can electronically deposit money from their bank accounts straight into your business’s bank account, and you can return ACH payments to them in the form of credits and refunds.

In the United States, an electronic money transfer method called ACH is used. Using your bank account to pay pals using Venmo or PayPal, paying your utility bill online using your bank account, or getting a direct transfer from your job are all examples of ACH payments.

Dwolla payment security: To further lower the risks of ACH returns and fraud, Dwolla checks client bank accounts and makes sure critical information can’t transit via your systems. Additionally, the business encrypts all data transferred over its network to safeguard the privacy of both you and your clients.

Dwolla payment API: Dwolla API reference material. You can link your program to the financial infrastructure using this API to transfer money, store money, confirm client IDs, and verify bank accounts.